Mutual fund investments: Recent increases in investments in specific fund categories and schemes have prompted concerns. Investors flock to funds with strong previous returns, sometimes neglecting the accompanying significant risks. Sebi wants to guarantee that investors evaluate not only performance but also the dangers involved. Sebi believes that risk-adjusted returns provide a more comprehensive perspective of fund performance. Will it eventually benefit mutual fund investors?

Sebi has once again highlighted the danger in mutual funds. It has suggested that all mutual funds must display risk-adjusted return, not merely return. This risk-adjusted return will be recorded as a ‘information ratio’.

In essence, the information ratio compares a fund’s excess return to its excess risk and shows how well it performs in relation to its benchmark. It is computed by dividing the tracking error (the active return’s standard deviation) by the active return, which is the fund’s return less its benchmark index. Better risk-adjusted performance, or how well a fund outperforms its benchmark after taking volatility into account, is indicated by a larger ratio.

Why is the Sebi pushing for this disclosure now? Recent increases in investments in specific fund types and schemes have prompted alarm. Investors flock to funds with strong previous returns, sometimes neglecting the accompanying significant risks. Sebi wants to guarantee that investors evaluate not only performance but also the dangers involved. Sebi believes that risk-adjusted returns provide a more comprehensive perspective of fund performance.

Certain funds have incurred greater risk in order to yield bigger returns.

Currently, not all fund companies report risk-adjusted returns. The Sebi has noted that 33 of the 39 investment institutions conducting equity programs publish the data. Only 27 of the 36 fund institutions that administer hybrid schemes provide their risk-adjusted return data. Furthermore, AMCs do not adopt a consistent technique for computing risk-adjusted return or the frequency of NAVs used for this purpose. Sebi intends to standardize the measure in the form of an information ratio.

Will this new disclosure help you better understand the underlying risk? It is true that focusing just on a fund’s historical performance might be deceptive. Two funds may have achieved comparable returns while taking different risks to achieve those returns. Alternatively, a fund that is considerably outperforming the others may be assuming a far bigger risk. A fund that takes on less risk will normally give a more steady return, even if it does not generate a large return. Another fund may occasionally provide record-breaking returns while producing dramatically differing results along the way.

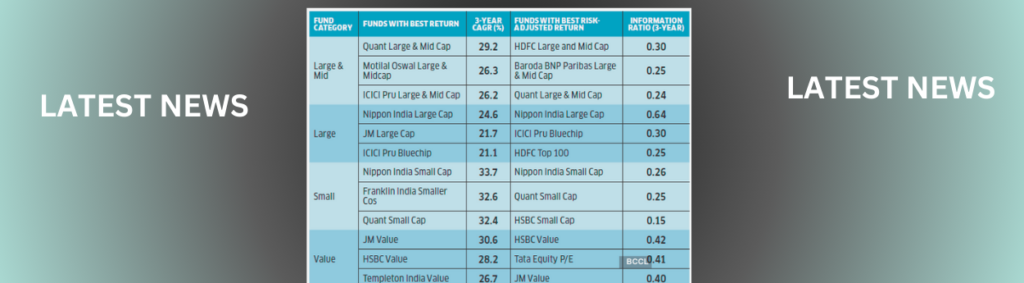

You have a good idea of what you are getting into if this is quantified. Quant Large & Mid Cap, for example, has beaten its competitors in the last three years among large- and mid-cap funds, although it lags behind HDFC Large & Mid Cap and Baroda BNP Paribas Large & Mid Cap in terms of risk-adjusted return, as measured by the information ratio. Comparably, JM Value has led the value fund charts, but in terms of risk-adjusted return, it lags behind Tata Equity P/E and HSBC Value. It’s evident that the two chart-toppers have performed better but more inconsistently.

Investors are, of course, no strangers to risk measurements. Fund factsheets already include metrics like the Sharpe ratio and standard deviation. A fund’s standard deviation indicates how volatile it is by measuring the dispersion in its return. The Sharpe ratio accounts for volatility and compares the return of a fund to the risk-free rate of return. Of course, there are limitations to both of these measurements.

Although information ratio has applications, most investors won’t find it useful, according to experts. “Most of these ratios are very technical and cannot be interpreted by lay investors,” says Rushabh, Founder of Rupee with Rushabh Investment Services. According to Vidya Bala, Head of Research at Primeinvestor.in, there is an abundance of information available to investors. A fund’s Sharpe ratio may occasionally show a higher value than its information ratio. The investor finds it difficult to determine which is more important, according to Bala. The founder of Invest Mutual, Mahesh Mirpuri, continues, “These ratios are not very useful because fund managers change all the time.” When a fund manager leaves, the ratios become less meaningful very fast. The fund house procedure and investment approach are more important, he claims.

Furthermore, information ratio is not without flaws. It is possible to determine if a fund beat its benchmark when taking risk into account, but it is not possible to pinpoint the exact method used to achieve the outperformance. The information ratio will be insufficient to present the whole story. According to Desai, “it won’t tell you if it was pure luck or the fund’s investing style that clicked at that time.” For many years, growth-style funds outperformed value funds, but then the market turned its preferences toward value, putting the former in jeopardy. No ratio can adequately convey the performance’s cyclical nature. Experts maintain that the rolling return of a fund provides a more accurate overall indicator of the fund’s performance. It can show how regularly and by how much the fund outperformed.